Medicare Premiums and Deductibles for 2025

We need to take a better look at how the changes in Medicare payments, deductibles, and other costs can affect your healthcare budget in 2025. It is important to know these prices whether you are signing up for Medicare for the first time or looking over your current coverage choices.

Medicare can be hard to understand, but it does not have to be impossible. This detailed guide will show you how much each part of Medicare will cost in 2025. This includes Part A (Hospital Insurance), Part B (Medical Insurance), Part C (Medicare Advantage Plan) and Part D (Prescription Drug Coverage). You will have a better idea of what to expect and how to make plans for 2025 Medicare costs after reading what follows.

2025 Medicare Costs of Part A: Hospital Insurance

Part A of Medicare pays for hospital stays, care in a skilled nursing center, hospice care, and some home health care services. Part A is premium-free for most people, which means they do not have to pay a monthly fee to be insured.

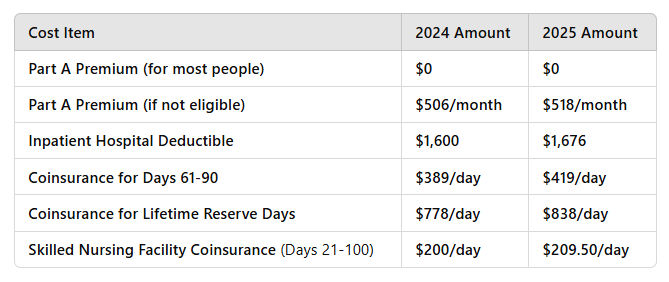

Eligibility for Premium-Free Part A

If you or your partner have worked and paid Medicare taxes for at least 10 years (40 quarters), you can get Part A for free. You can still buy Part A even if you have not worked enough to get it for free, but the price will go up to $518 a month in 2025.

Part A Costs in 2025

The main costs for seniors with Part A that do not require a payment are the deductibles and coinsurance. Here is how much it will cost in 2025:

- Inpatient Hospital Deductible:

It costs $1,676 to cover each benefit period in 2025. This is how much you have to pay for your hospital stay before Medicare starts to pay for it. Over-the-counter medicines will cost more every day if you stay in the hospital for more than 60 days.

- Coinsurance for Hospital Stays:

After meeting your deductible:

- Days 1-60: No coinsurance.

- Days 61-90: You’ll pay $419 per day.

- Lifetime Reserve Days: For days 91 and beyond, you pay $838 per day (up to 60 days in your lifetime).

- Skilled Nursing Facility Coinsurance:

For stays in a skilled nursing facility:

- Days 1-20: No cost.

- Days 21-100: You’ll pay $209.50 per day.

- After day 100, you’ll be responsible for all costs.

This information helps you prepare for possible stays in a hospital or get a skilled nursing facility at home, which can cost a lot if you are not informed.

Medicare Part B: Medical Insurance

Medicare Part B includes care that you get at home, visits to the doctor, medical products, and services that keep you healthy. Unlike Part A, Part B does come with a monthly premium, which is based on your income.

Part B Premium in 2025

The standard monthly premium for Medicare Part B will be $185 in 2025, which is an increase of about $10.30 from the previous year. This premium amount is deducted directly from your Social Security payments if you receive them.

Part B Deductible and Coinsurance

In addition to the premium, you’ll have to pay an annual deductible of $257 in 2025. Once you meet the deductible, Medicare will pay 80% of the Medicare-approved amount for most services, and you’ll be responsible for the remaining 20%.

It is important to read the details of each service because some, like physical therapy, medical equipment, or outpatient surgery, may have extra costs.

Income-Related Monthly Adjustment

You will have to pay a bigger Part B fee if your income is above a certain level. This is based on your modified adjusted gross income (MAGI) from 2023. IRMAA stands for “Income-Related Monthly Adjustment Amount.” The extra monthly fees run from $259 to $628.90, based on your income.

Medicare Part C: Advantage Plans

You can choose Medicare Advantage plans instead of Original Medicare (Parts A and B). Many of these plans come with extra benefits like coverage for eye, dental, and hearing aids. A lot of them also come with coverage for prescription drugs (Part D).

It depends on the plan, but Medicare Advantage plans usually have low out-of-pocket costs and low annual premiums. But you should look at every detail of each plan, like the list of doctors, the amount of coverage, and the drugs that are covered, to make sure it fits your needs.

Medicare Part D: Prescription Drug Coverage

You can get help for prescription drugs through Medicare Part D, whether you have a separate Part D plan or a Medicare Advantage plan (Part C) that covers prescription drugs.

Part D Premiums in 2025

The national base premium for Medicare Part D in 2025 will be $36.78. However, this amount can vary depending on the plan you choose. There are plans that offer more benefits, but the cost may be higher.

Income-Related Premiums for Part D

You will have to pay more for prescription drug coverage if you make more money. No matter how much money you make, your Part D rates will run from $13.70 to $85.80 in 2025. These payments are added to the usual monthly cost for your Part D plan.

The Donut Hole (Coverage Gap)

The “donut hole,” which is part of Medicare Part D, is a funding gap that starts after you and your plan have spent a certain amount on approved drugs. When your out-of-pocket drug costs reach $4,660 in 2025, you will enter the “donut hole,” where you will pay a higher amount for your medications until they hit $7,400. The catastrophic coverage starts at that point, and all you have to do is pay a small amount or copayment.

Late Enrollment Penalties

It is best to sign up for Medicare as soon as you become qualified. You might have to pay a fine for life if you wait too long to sign up for Part B or Part D without having good coverage, like through the company you work for.

- For Part B, the penalty is 10% of the monthly premium for each 12-month period you could have been enrolled but weren’t.

- For Part D, the penalty is 1% of the national average monthly premium for each month you delayed enrollment.

Medicare Supplement Insurance, or Medigap, helps pay for some of the costs that Original Medicare does not cover, like copayments, coinsurance, and deductibles.

There will still be a lot of different coverage choices for Medigap plans in 2025. These plans usually have an extra monthly fee on top of your Part B fee, but they keep you from having to pay a lot for medical bills.

Final Thoughts:

In 2025, Medicare costs will depend on your health needs, financial status, and whether you choose Original Medicare or a Medicare Advantage plan. It is essential to understand these expenses in order to properly plan for your healthcare budget and prevent any unexpected expenses in the future.

If you need specialized help figuring out Medicare, LMS Insurance Group is here to help. We can help you look at your choices and find a plan that fits your goals and budget for 2025 and beyond.